4th Quarter Rally?

The month of September has thus far been a rough one for financial markets, unfortunately continuing the downward trend we saw in August. Heading into today, the S&P 500 is down nearly 4% in September while bonds have declined 2.5%. The majority of this month’s decline has come on the heels of last week’s FOMC meeting, where the Federal Reserve announced their decision to leave interest rates unchanged. However, in their post meeting press conference the Fed implied that rates are likely to stay “higher for longer.” Judging by the performance of the stock market since that Fed meeting, many investors, who had been hoping to hear messaging about potential future rate cuts, were not pleased.

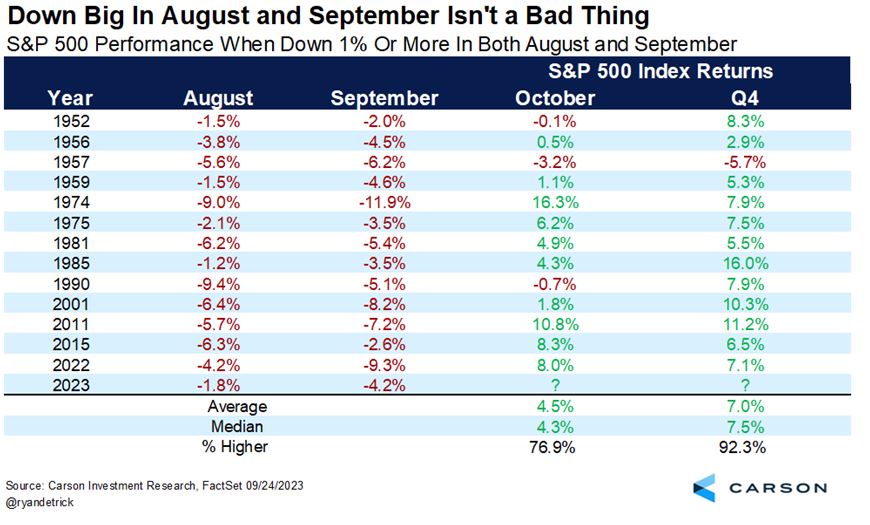

Before I address the Fed, let’s take a moment to discuss the recent market pullback that is now nearing on two months. With all the headlines out there threatening to derail the economy – government shutdown, UAW strike, rising oil prices – it’s natural for investors to be feeling a lot of angst these days. However, taking a step back a bit it’s important to consider that the stock market had an incredible run during the first 7 months of 2023 with the S&P 500 gaining more than 15%. So to see the markets take a breather here is not uncommon, especially during the late summer/early fall months which have historically been a weak time of year. Speaking of history, if we let that serve as a guide for what the remainder of 2023 might hold, there’s reason for optimism in our view. Since 1950 there have been 13 instances when stocks (S&P 500) were down more than 1% in both August and September. In 12 of those instances, the market went on to post some pretty significant gains in the 4th quarter…

That’s good for an average 4th quarter gain of 7%. Of course, past performance is no guarantee of future results. The one outlier in the chart above is 1957 where the market was not only down in August and September, but continued heading lower throughout the remainder of the year. But then again that was during the Eisenhower recession, a nasty one that lasted nearly a full year. Today we have not only averted a recession (thus far) but economic growth projections have actually been increasing!

Speaking of growth projections, let’s get back to the Fed. While investors were bemoaning the fact that the Fed left the possibility of future rate hikes on the table, they may have overlooked the reasons as to why. Most importantly, the Fed increased their real GDP growth projection for 2023 from 1% to 2.1%. Not only did the Fed boost their projections for GDP this year, they also increased their 2024 GDP growth forecast for 2024, while lowering their forecast for the unemployment rate. That is a huge shift and an acknowledgement that the U.S. economy is strong. The take here is that the “higher for longer” message from the Fed has less to do with inflation and more to do with a stronger economy.

If inflation projections are coming down, and economic growth projections are going up, why is the market struggling? A big reason is simply because the market was due for a breather. As I mentioned above, the market had a great run during the first seven months of 2023, and unfortunately markets don’t go up in a straight line. But another reason is that market participants simply aren’t buying into the Fed’s projections for stronger economic growth. A large majority of investors today have never experienced a higher interest rate environment so they’re operating on the only playbook they know: high rates = inflation problem = bad for economy = bad for stocks. And this is true if inflation persists higher and remains a problem. But as we have mentioned several times, inflation is on a clear glidepath lower. Though the Fed was seemingly reluctant to admit it, they acknowledged this fact by lowering their inflation projections for both 2023 and 2024.

So we have a disconnect between market expectations and the Fed’s long-run expectations that will eventually have to be reconciled. Until that happens, markets are likely in store for continued volatility. If inflation continues to head lower and consumer spending remains strong, investors may soon start to buy into the growth story.

Thank you for your continued confidence and support. As always, if you have any questions, we’re just a phone call or email away.

Brian